A automação digital das empresas de seguro de vida de Luxemburgo está progredindo rapidamente

06min

1 A positive regulation to support an attractive market

Luxembourg regulation for Life Insurance contacts offers a very attractive set of characteristics that have supported the local development of the biggest companies in the sector over the last decade and at SuisseTechPartners we are delighted to say that we fully support such Life Insurance Companies through deployment of our global product “PMPlus”.

That strength of this industry resides in the following characteristics:

– Close supervision of such schemes by the local regulator, the “Commissariat Aux Assurances” (ACA)

– A clear segregation of duties between the Life Insurance company and the Depositary Bank; holding the assets to guaranty full protection to the contract holder against a bankruptcy or other such events.

– The status of “first ranking creditor” for the contract holder

– The capacity to hold contracts in other currencies than the Euro

– The permanent availability of contract assets as the Life Insurance Company – i.e. the Company cannot block asset withdrawals

– The contract holder can freely designate the ultimate beneficiaries of the contract to receive benefits upon completion

– The flexibility to opt for different types of underlying assets and the flexibility of the investment guidelines indexed on the size of the contract and the wealth of the contract holder,

– The taxable position (such as an unrealized gain) within the contract is not impacted by a change of portfolio manager

– People non residing in Luxembourg will not be taxed on the contract signed in Luxembourg, only according to their home country tax law At the end of 2023 the total assets of such Luxembourg Life Insurance contracts amounted to 222 billion euros according to ACA statistics, and 79 % of total assets were invested in Unit Linked contracts benefiting of the expertise of Luxembourg in fund distribution.

The regulation is de facto creating a segmented market with five categories of investors (N, A, B, C, D) defined by the maximum amount of the contract and depending on the movable wealth of the owner. For each category there are clear investment guidelines by asset type. Yet, the level of expected services will be driven not only by the profile of investors but by the industry competition as well.

As seen above, most of the assets are invested in Unit Linked contracts – investing in external and internal funds – and one could imagine the offering for the majority of the contracts to be straightforward and uniform. Most Life Insurance Companies have suppressed entry fees and the yearly management fees tend to be very similar across Companies. The key differentiators are on the solvency of the company , the variety of investment funds proposed for subscription ( UCITS , PE Funds, soon ELTIFS) and the quality of operational services ( execution, on line arbitration, …..)

For the wealthier and potentially more sophisticated investors the main factors of success will be based more on the range of investible assets, the capacity to monitor investment guidelines and the manager’s performance.

2 A market with new and growing needs

To some extent, the Life insurance markets is experiencing the same revolution as the Banking industry resulting from several key requirements:

– The digitalization of their processes to improve the client experience and satisfaction. More and more Investors want to access their portfolio on-line with more frequent valuations and the capacity to make timely investment decisions.

– The capacity to offer a wider variety of financial instruments requested by investors at a time when interest rates were particularly low. Life Insurance Companies have to work in coordination with Depositary Banks who are facing the same difficulties to serve their clients that wish to invest in digital or private assets

– The demand for more sophisticated reports to monitor the actual performance and adequacy versus the investor guidelines. Portfolios attached to a Life Insurance contract can be of significant size and sophisticated. Investors do expect to get a clean reporting with integrated performance and risk data

– The rise of ESG as a critical consideration, which is a challenge across all steps of the portfolio management and the reporting processes

– The need to automate their processes to reduce operating costs and risks. Obviously Life Insurance Companies and Depositary Banks share processes but the Life Insurance Company is ultimately responsible vis à vis the investor and owns the assets impacting their balance sheet.

Processes like portfolio rebalancing, fund execution, custodian reconciliation or portfolio valuation should be highly automated

– the need to monitor cash flows in a consistent way to optimize their treasury and associated risks in a rising interest rate environment

– the willingness to increase their oversight on Depositary Banks and to control portfolio valuations as not only are they required to provide their clients, but it also does impact their technical reserves

– The need for full multicurrency valuations of the underlying assets and the portfolio itself if denominated or invested in a currency different from the Euro or other base currency.

3. Life Insurance companies do have solutions to face their operating / servicing challenges

The evolution of the Life Insurance market is obviously a source of opportunity for the future as it is attractive for the end investors in many aspects. Though, this evolution generates strong operating challenges for the Companies who have to adapt to the investor needs, the regulation and the evolution of their competitors:

– Life Insurance companies have over the years created links with Depositary Banks who are facing difficulties dealing with new asset classes like private or digital assets in a consistent way, in order to feed data back to the Life Insurance Company. There is a need to streamline these connections as much as possible in order to reduce manual processes.

– Their own IT architecture might be somewhat obsolete in respect of digitalization, new classes of instruments, heightened service expectation, and the need for efficient data management. At the same time it is costly and complex to redevelop brand new platforms while competition and market evolve

– They need more and more to develop an independent set of controls to oversee the activities of the Depositary Bank versus a simple reliance on data received at month end which may not be sufficient anymore.

The needs of Life Insurance companies do not differ much from those of other asset/wealth managers in the sense that they need to receive comprehensive positions and transactions files from the custodian banks, reconcile these data and then provide appropriate reporting. Part of the complexity is that such transactions are generally high volume and smaller ticket-size which can easily overwhelm processes originally designed for lower-volume and higher ticket sized institutional business.

The evolution of client expectations, and of the complexity of portfolios makes it less and less easy to rely only on the custodian bank data. The Insurance Company must have the capacity to have their own independent set of data which they can reconcile internally to multiple external providers (custodian, fund administrators or market data vendors…)

This is where the new technology platforms launched on the market and mostly developed by financial technology (Fintech) firms do offer efficient solutions to meet these requirements and face most of these challenges.

The combination of recent technology components (programming languages, reporting component, web services, cloud services, machine learning,…) such as those available in SuisseTechPartners’ PMPlus application provide agile solutions which are functionally rich and easier to deploy with a modular approach if needed. Control of data flow by automated filters, alerts and consequent exception processing/dashboards, streamline the operating model to a more manageable dimension.

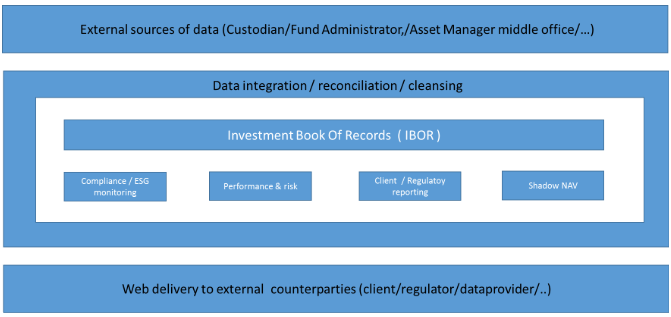

The following diagram shows the functional design of such platforms in which the nucleus is the Investment Book of Records (IBOR) which captures all transactions and positions for a given portfolio / investment structure.

O objetivo da criação do IBOR é múltiplo:

- Criar uma visão consolidada dos ativos com base em uma aquisição eficiente de dados de várias fontes

- Reconciliar várias fontes para garantir a consistência da construção da posição

- Reparar posições que não correspondem à(s) fonte(s) de dados utilizada(s)

- Enriquecer as posições com dados não fornecidos por fontes externas e necessários para o processamento subsequente.

Depois que as posições do IBOR são confirmadas, elas podem ser reutilizadas de forma consistente para funções como monitoramento de conformidade ou análise de desempenho, pois as informações básicas são as mesmas para todos os cálculos e relatórios.

A lógica da IBOR parece atraente, mas é essencial verificar se os dados injetados estão totalmente reconciliados e limpos para obter um conjunto limpo de posições precisas antes de fazer qualquer cálculo sofisticado e gerar relatórios.

A melhor maneira de construir a posição é com base em transações individuais que podem ser integradas em qualquer estágio após o nível de execução/confirmação. Em seguida, as posições podem ser reconciliadas com fontes externas, como o Middle Office do Asset Management, o Custodiante e/ou o administrador do Fundo.

Alguns poderiam dizer que o conceito de IBOR já existe há algum tempo e isso é correto. A diferença é que hoje os novos componentes tecnológicos permitem que as plataformas recém-desenvolvidas sejam muito mais poderosas e ágeis em sua capacidade de desenvolver novas funções, interagir com novas contrapartes ou fornecer relatórios aprimorados e definidos pelo usuário. Esses elementos são essenciais para otimizar o processo de implementação.

O segundo elemento importante é que a maioria dos participantes precisa cobrir o mesmo universo de investimento composto por ativos custodiados e não custodiados. O principal fator de diferenciação entre eles é o orçamento disponível para criar uma solução IBOR. É nesse ponto que plataformas como o PMplus, baseadas em nuvem e com ampla conectividade de interface oferecida em um modelo SaaS, podem ser implementadas rapidamente. Além disso, um recurso seguro para vários locatários contribui para uma solução mais econômica para todos os tipos de orçamento.

4. Conclusão

O sucesso desse setor e o crescimento contínuo dependem da automação em larga escala, por meio da rápida implementação de SaaS, da ampla conectividade existente, da filtragem e da correspondência avançadas de transações, do gerenciamento de exceções/painéis de controle e de alertas de tempo crítico.

Na SuisseTechPartners, criamos os processos e os recursos necessários para dar suporte a esse setor e teremos o maior prazer em discutir esse tópico com você e mostrar como podemos ajudar sua empresa a adaptar a arquitetura de tecnologia nesse ambiente em rápida evolução.